This is a guest post by Phil Hill. Phil Hill is executive vice president of Delta Initiative and has been consulting in educational technology for over 8 years, with a strong focus on the LMS market. He is also the founder of HBO Systems, which merged operations with Delta Initiative in 2008. Phil is known to many in the educational technology community for some info graphics that help people see the broader trends and issues with the technology markets. You can follow Phil on Twitter at @PhilOnEdTech or on his main blog at http://www.deltainitiative.com/index.php/phils-blog.

I have argued in previous blog posts on the Blackboard acquisition that their position of being a safe bet is now gone, they are picking up only a handful of new LMS clients, while they are losing hundreds of LMS clients per year. The theme behind these observations is that Blackboard’s future prospects “are having and will have a major impact on the overall LMS and educational technology market, affecting educational customers as well as technology vendors and their investors. If you misread Blackboard’s strategic direction, you might misread the upcoming changes in the educational technology market.”

Put another way, as Lou Pugliese commented in a post by Michael Feldstein on the LMS Market –

Typical disruptive markets (Clay Christiansen) are repeatable events exist where (a) over-served customers consume a product or service but don’t need all its features or functionality (b) there is broad based industry concern about the effective use of overly complex, expensive products and services (c) features that are not valued and therefore are not used and (d) decreasing price premiums for innovations that historically created value but in the current market are now irrelevant. The street will eventually see it this way no matter how you NPV a business’s customer base. . . . I would argue that there is an exact parallel here and the education market is not immune to the same disruption experienced in other markets.

What I believe we are seeing in 2011 is a transition to a market no longer dominated by Blackboard and other players’ reactions to Blackboard. This new market that is emerging will look quite different from the market we have seen for the past 6 – 8 years, and we should no longer view this as an evolving market, but instead view it as a market being disrupted, with new competitors and new dynamics.

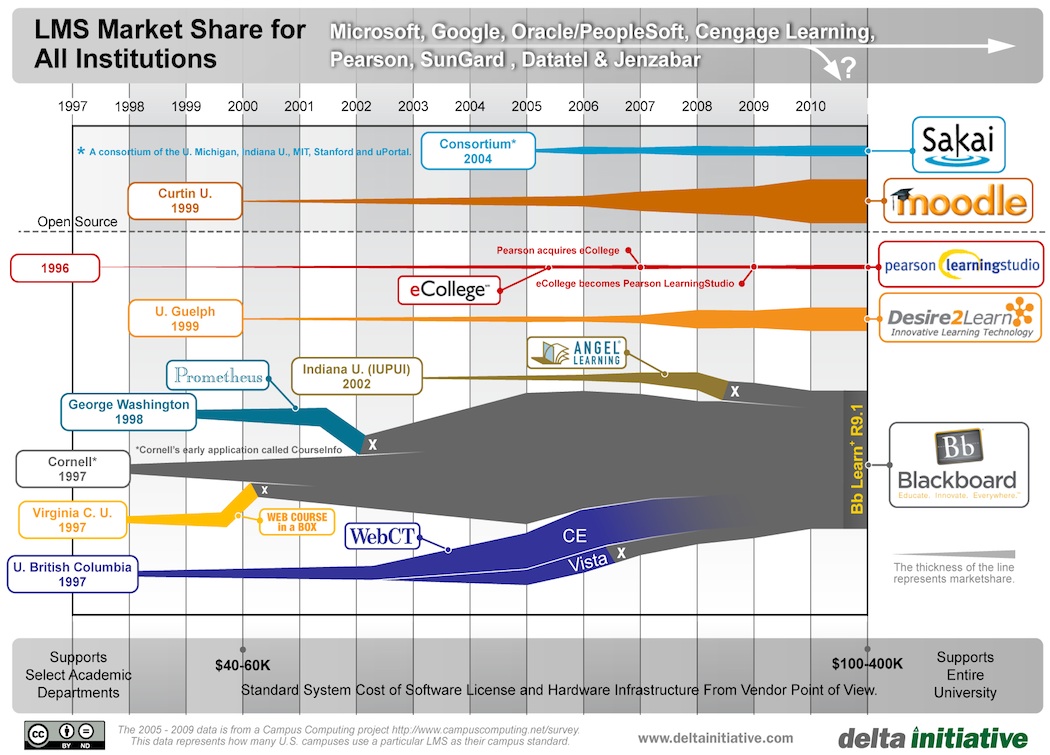

LMS Market History

For the past decade, the LMS market has evolved from providing tools that were purchased at the departmental level to enterprise-class systems purchased at the institutional or even system-wide level. However, since about 2004 the market has been fairly consistent, dominated by Blackboard corporate strategy.

Blackboard went public in 2004, signaling a real market worth of investors’ attention. In 2005 – 2006, the market was dominated by Blackboard’s acquisition of WebCT, the number 2 player in LMS, resulting in a somewhat extended Department of Justice approval cycle. Starting in 2006, Blackboard was awarded the infamous ‘138 patent and subsequently filed suit against Desire2Learn, the new number 2 player in LMS. About this same time, open source started to become a viable alternative to proprietary systems in general, and Blackboard in particular, in the form of Moodle and Sakai. From 2006 – 2009, open source became fully established for campus-wide or system-wide LMS deployments. In late 2009, Desire2Learn successfully fended off Blackboard patent lawsuits, ultimately resulting in all 38 claims being ruled invalid by a US Court of Appeals. On the heels of these efforts in 2009, Blackboard purchased Angel, taking another competitor out of the market.

Whatever the merits of each individual event or situation, the point is that the market was dominated by the Blackboard corporate strategy and the rest of the market’s reactions to such moves. The market of these years can be summarized by the following graphic.

Transition

From my viewpoint in 2011, the market has essentially moved beyond Blackboard as the dominant player driving most of the market dynamics. There are several factors that have hastened the changes that we are now seeing.

- Blackboard has run out of LMS companies to purchase or target with patents. WebCT, Angel and Prometheus no longer exist – and Desire2Learn is not available for sale. Blackboard’s acquisitions since 2009 have targeted complementary technologies rather than direct competitors.

- No one questions the validity of the open source model as a credible solution for ed tech.

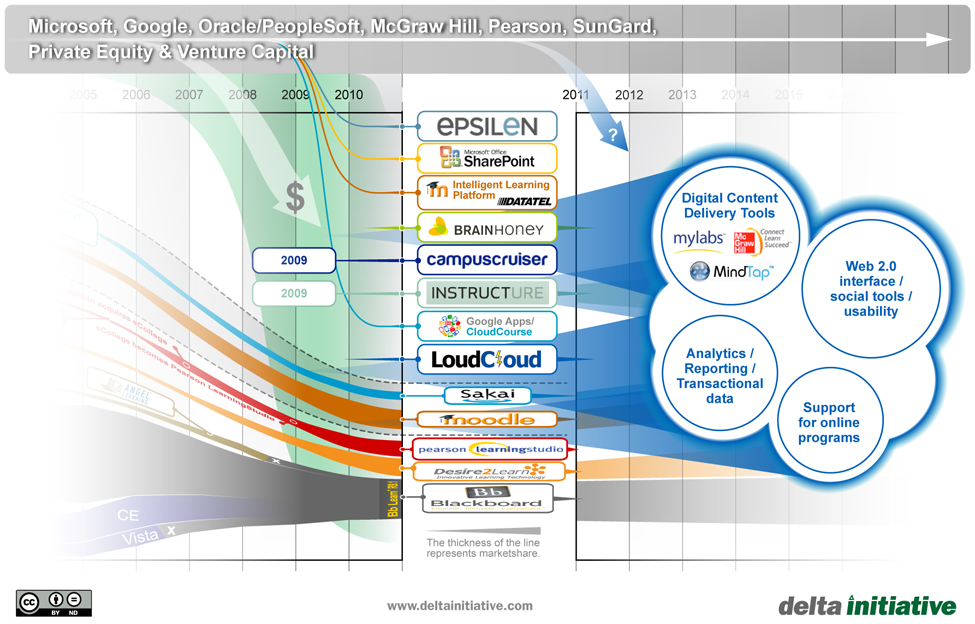

- New investment is coming into the market in the form of private equity buyouts, venture capital funding, and strategic company acquisitions. The result is that there are more options available today than there were just two years ago.

Trends for the Future

The question is, what will the LMS market that is emerging from these changes look like? No one can know for sure what will happen over the next 3 – 5 years, but I do think there are some key trends that are worth understanding.

- The market is more competitive, with more options, than it has been for years. Instructure is a real player that has shown that it can win against established LMS vendors with big wins in Utah and at Auburn. LoudCloud has new clients at CEC, Grand Canyon U and an unreported win at a public state university. BrainHoney won at BYU. Pearson LearningStudio has major wins at Arizona State and Columbia online programs. Desire2Learn has roughly doubled in size in the past year. Moodle and Sakai, including through providers such as MoodleRooms and rSmart and Unicon, continue their impressive wins in the market.

- Related to the above, there is a trend towards software as a service (SaaS) models for new LMS solutions. The SaaS model offers some compelling advantages in terms of deployment time and ability to mine and report transactional data that might not be possible with other approaches. SaaS is not a panacea, but this is a growing trend in the LMS market.

- Also related to the above, the market is demanding and getting real Web 2.0 and Web 3.0 advances in LMS user interfaces and functionality. We are starting to see some real improvements in usability in the LMS market.

- The lines are blurring between content delivery systems (e.g. Cengage MindTap, Pearson MyLabs, etc) and LMS. Content delivery and ability to keep students engaged within the content will drive much of the broader ed tech market. This integration of markets is being seen as a strategically important issue for institutions, particularly for online programs.

- Along those same lines, it is also interesting in what is not being seen as a strategic blurring of lines – between LMS and student information systems. It seems that IMS standards and other efforts might be commoditizing this integration – LMS / SIS interaction is still important, but it is not a strategic differentiator in the market in the same way that LMS / content interaction is proving to be.

- Analytics and data reporting are not just aspirational goals for LMS deployments, but real requirements driven by real deadlines. In the past, institutions liked to talk about analytics, reporting and learning from data, but there were few real projects driven by real needs. With regulatory changes for online programs, changes in state funding models (e.g. Arizona and other states moving to outcomes-based funding of public institutions rather than enrollment-based funding), and general budget changes in general – the need for real, actionable data coming out the LMS is now critical and likely to start producing more results.

Of course these observations are subjective, but it is becoming quite clear that the LMS market of next year will look quite different than the LMS market of just 2 years ago. I would also expect to see new disruptions and new competitors emerge within the next year or two.

Phil

Strong and thoughtful post. Thank you.

One additional trend that I’m seeing is a lot of interest in Microsoft SharePoint as a learning platform. It’s available very cheaply in education and provides a robust environment to authenticate/authorize students, instructors and other stakeholders and it’s a great platform to deliver learning and assessments from and allow collaboration. SharePoint does need some investment to use, it’s not an install and it all works for you system, but it’s a lot more flexible and integratable with than an LMS.

I suspect think that the cloud-based Office 365 which includes SharePoint, although initially targetted more at businesses, could be very attractive to colleges and universities.

I agree with the interest and concept of using SharePoint in higher ed for LMS function (and somewhat the content management function). What I haven’t seen (yet) is real traction, based on institutional adoption. It will be interesting to see if the trend you’re seeing develops into real usage.

SharePoint can be less visible than other systems as it gets customized. Also often gets used for admin and only a bit for learning.

See http://blog.sharepointlearn.com/2011/03/11/78-of-universities-use-sharepoint-but-mostly-not-for-learning/ for evidence that 3/4 of UK universities use SharePoint though mostly not for learning.

Thanks for this good post.

I misses the Open Source System: ILIAS from Germany.

You did n’t show it in the graph. Is it forgotten?

In august is a conference in Bern where the new steps will be shown.

http://www.ilias-conference.org/index.php/home.html

I’m missing our product Sharepoint LMS – which might be the fastest growing LMS globally. Built upon Sharepoint and fully integrated with the Microsoft stack it takes adavantages of all Microsoft product features including out-of-the box integration to Live@edu.

Sharepoint itself is not a solution – it needs to be combined with a learning platform in top of Sharepoint. Sharepoint LMS is the most comprehensive learning platform on Sharepoint today.

More educational institutions realize that an integrated solution is necessary. Eg. to Intranet, extranet and internet become very urgent. By using Sharepoint & the microsoft stack all component in a total solution can be fully intergrated on the same platform – using the same user database (Active Directory)

As this analysis doesn’t cover Sharepoint LMS – feel free to contact us from our website – we will be happy to answer all questions.

Given the ubiquitious nature of WordPress, it may become a player in the opensource LMS space when enhanced with the BuddyPress plugin, and others.

Great to read your comments on LMS trends. I am interested on your perspectives on a Sharepoint based LMS which does not appear in your graphics. We use Scholaris which has its origins in Western Australia, grew nationally and is in the British and Canadian markets. We like the integration of functions. Our school has parent access to attendance, assessment and virtual classrooms.

A good summary!

You say: “It seems that IMS standards and other efforts might be commoditizing this integration – LMS / SIS interaction is still important, but it is not a strategic differentiator in the market in the same way that LMS / content interaction is proving to be.” I suggest that LMS/SIS integration will be a game changer, especially if the pattern which Bb set as the ‘big-boy’ in the market in its acquisions, continues. Read between the lines: Bb is purchased by Providence Equity Partners who just ‘happen’ to also own what many would say is one of the two top SIS systems — Banner (part of SunGard’s suite).

Interesting take on LMS / SIS, but note that Providence is in the middle of selling SunGard Banner. https://eliterate.us/sungard-he-and-blackboard-acquisitions-compare-and-contrast/

We’re both projecting into the future, but I maintain that LMS / SIS integration is going the commodity route. It will be interesting to see whether this view holds, say 2 years in the future.

To be clear, Providence only owns a small minority stake in SunGard.

Excellent article Phil, well done!