I have previously written about the deeply flawed Brookings Institution analysis on student debt with its oft-repeated lede:

These data indicate that typical borrowers are no worse off now than they were a generation ago …

Their data is based on the triennial Survey of Consumer Finances (SCF) by the Federal Reserve Board, with the report based on 2010 data. With the release of the 2013 SCF data, Brookings Institution put out an update this week on their report, and they continue with the lede:

The 2013 data confirm that Americans who borrowed to finance their educations are no worse off today than they were a generation ago. Given the rising returns to postsecondary education, they are probably better off, on average. But just because higher education is still a good investment for most students does not mean that high and rising college costs should be left unquestioned.

This conclusion is drawn despite the following observations of changes from 2010 – 2013 in their own update:

- The share of young (age 20 – 40) households with student debt rose from 36% to 38%;

- The average amount of debt per household rose 14%;

- The distribution of debt holders rose by 50% for debt levels of $20k – $75k and dropped by 19% for debt levels of $1k – $10k; and

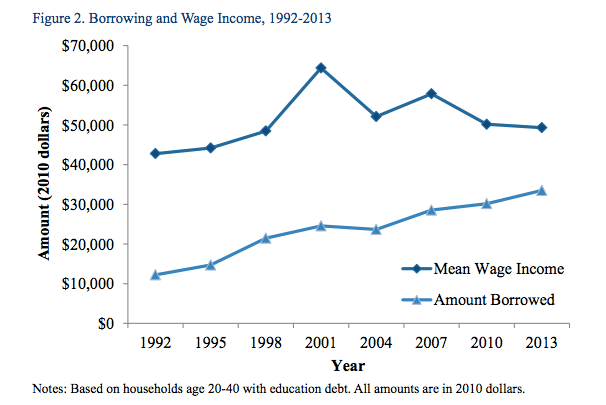

- Wage income is stagnant and same level as ~1999, yet debt amounts have risen by ~50% in that same time period (see below).

Brookings’ conclusion from this chart?

The upshot of the 2013 data is that households with education debt today are still no worse off than their counterparts were more than 20 years ago. Even though rising debt continued to cut into stagnant incomes, the average household with debt is better off than it used to be.

The strongest argument that Brookings presents is that the median monthly payment-to-income ratios have stayed fairly consistent at ~4% over the past 20 years. What they fail to mention is that households are taking much longer to pay off student loans now.

More importantly, the Brookings analysis ignores the simple and direct measurement of loan delinquency. See this footnote from the original report [emphasis added]:

These statistics are based on households that had education debt, annual wage income of at least $1,000, and that were making positive monthly payments on student loans. Between 24 and 36 percent of borrowers with wage income of at least $1,000 were not making positive monthly payments, likely due to use of deferment and forbearance …

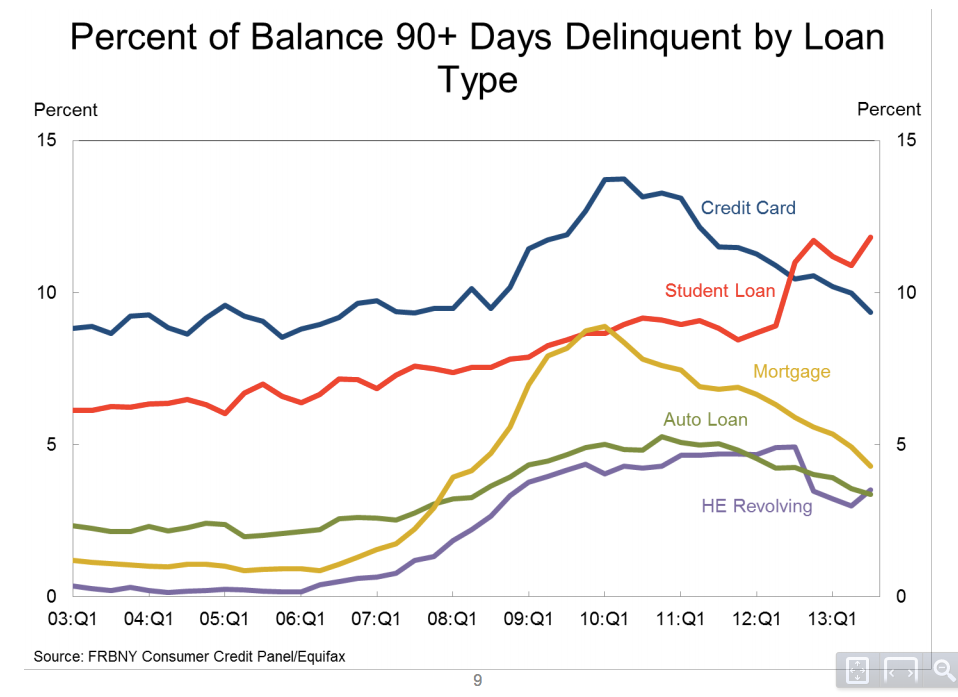

That’s what I call selective data analysis. In the same SCF report that Brookings used for its update:

The delinquency rate for student loans has gone up ~50% from 2010 to 2013!

How can anyone claim that Americans with student debt are no worse off when:

- More people have student debt;

- The average amount of debt has risen;

- Wage income has not risen; and

- The delinquency rate for student loans has risen.

None of the secondary spreadsheet jockeying from Brookings counters these basic facts. This ongoing analysis by Brookings on student debt is a farce.