Coursera’s stock dropped by about 30% on Wednesday in after-hours trading after their earnings announcement. The reason for the drop and the company’s own analysis of its financial performance are both instructive. MOOCs are more or less explicitly considered to be useful primarily as marketing tools rather than educational experiences. There’s reason to believe this is a bad idea for their university partners even from a financial perspective, never mind from university brand value and mission perspectives.

MOOCs are marketing tools

Higher Education Dive’s analysis of the stock drop is fairly representative of the reason for the decline:

Although Coursera reported overall revenue growth in 2022’s second quarter, revenue from the company’s degree segment declined 4% to $11.4 million, according to its latest earnings report.

Coursera Reports Revenue Declines in its Degree Business

This isn’t the whole story. The company missed analyst expectations for earnings growth and has guided lower on earnings growth going forward. But the conversation has focused on the degree program decline. Let’s look at what Coursera CEO Jeff Maggioncalda said about Coursera’s challenge in his own words during the company’s earnings call. Responding to an analyst question about problems in the “consumer” side of the business (which means degrees and certificates paid for by individuals rather than their employers), Maggioncalda said,

On the Consumer side, it’s interesting because the professional surge are still performing really well, particularly in North America. In Europe, it’s kind of more of a conversion rate challenge. And so, like Ken said, maybe it’s the same kinds of effects. You asked about activity levels, I don’t think that we’re seeing any notable difference in activity levels. It seems to be an even a lot of top of the funnel seems to be similar between Europe and other regions. I will say that, generally speaking, search volume for online courses and online degrees.

And this is not just on Coursera, which is general search volume is down. I think there’s sort of a bit of a the economy reopening and people doing things outside their house that we’re that we kind of see globally. And that probably is happening in Europe as well, but a lot of it sort of conversion rates on the Consumer segment in EMEA, and particularly Europe that we’re seeing.

Coursera, Inc. (COUR) CEO Jeffrey Maggioncalda on Q2 2022 Results Earnings Call Transcript

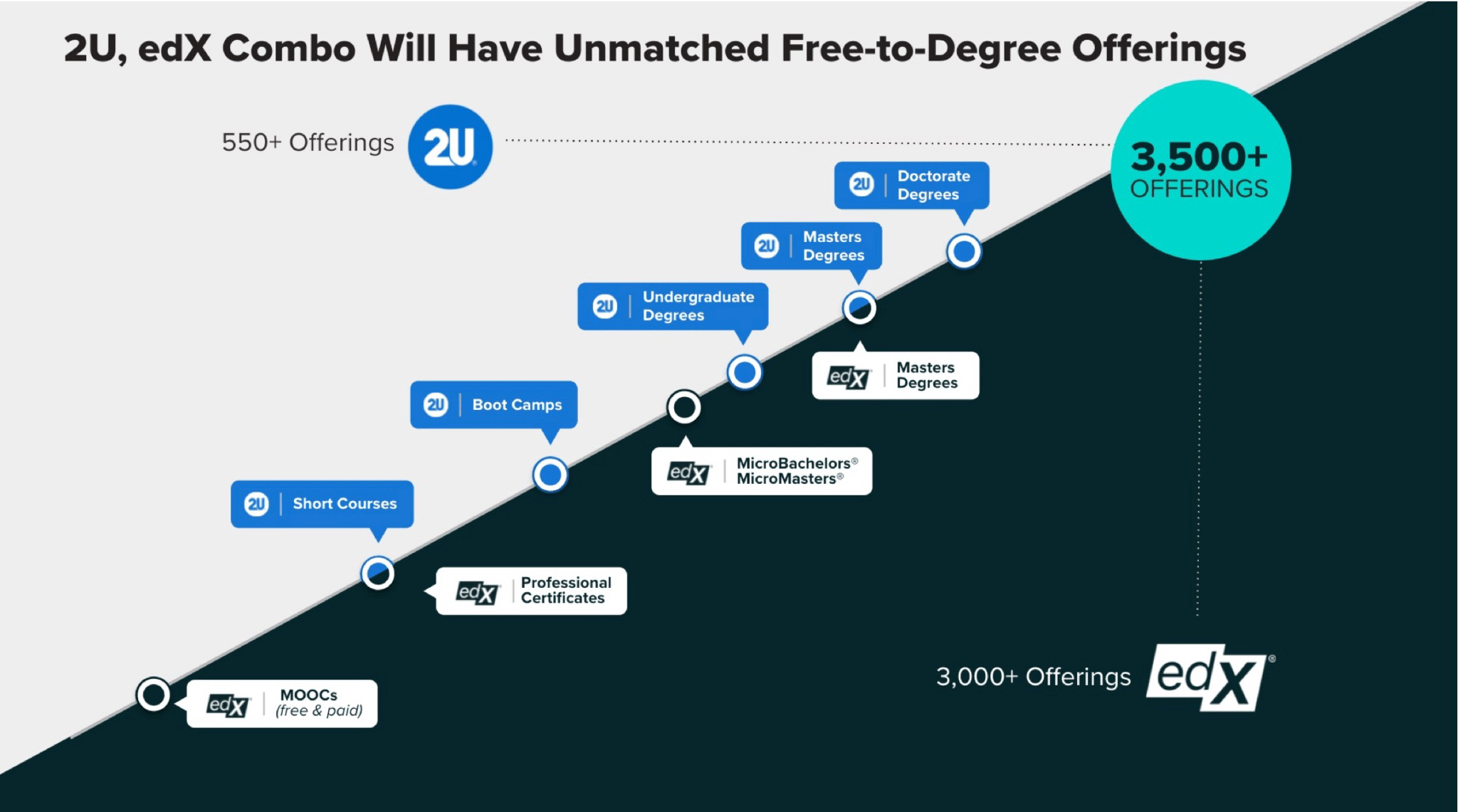

The key phrases in this excerpt are “conversation rate,” “top of the funnel,” and “search volume.” These are marketing terms. Free MOOCs are at or near “top of the [sales] funnel.” They are designed to identify and attract paying degree candidates. Meanwhile, 2U CEO Chip Paucek said a month ago in his company’s earning call that “[m]arketing investment decisions will be made at the platform level, aggregated across business lines with the goal of increasing the lifetime value of each learner.” The “platform” he’s referring to is EdX. The “lifetime value of each learner” means 2U intends to use the EdX platform to get learners to pay for more courses.

When 2U introduced its slogan “Free to Degree,” the company wasn’t describing their breadth of coverage. It was describing its sales funnel for getting students into paying degree programs.

We can see this mindset at work on the micro-scale by looking at the MOOCs produced by Coursera co-founder Andrew Ng, who now has a company called DeepLearning.AI that sells certificate programs on Coursera. Try the AI for Everyone certificate program. Don’t worry; you won’t have to pay anything to try it.

You’ll find it is a series of short, engaging, and mildly informative lecture videos by Andrew, each of which is followed by a quiz that anyone who was halfway paying attention could pass. This is absolutely terrible education. But that’s an unfair assessment. Because this “certificate program” isn’t really intended to be education.

Andrew Ng is at least twice as smart as me and has all the money in the world to pay high-quality learning designers. If his certificate program is not worth paying for, then the most obvious explanation is that he doesn’t really expect you to pay for it. It’s not a certificate program. It’s an infomercial designed to convince you that you need to learn more about AI. It’s the “top of the funnel” designed to “convert” you into a paying customer so that DeepLearning.AI can increase the “lifetime value” of you as a (future) enrolled and paying student in the company’s more extensive (and expensive) programs.

None of this is new but it’s oddly still news

In 2019 Justin Reich, possibly the single most prolific and widely respected researcher on MOOCs, co-published an article called “The MOOC Pivot: From Teaching the World to Online Professional Degrees.” The article’s abstract states, “[A]fter promising a reordering of higher education, we see the field instead coalescing around a different, much older business model: helping universities outsource their online master’s degrees for professionals.” Reich’s book Failure to Disrupt is similarly blunt (and well worth reading). MOOCs have become advertising tools to attract students into more lucrative degree programs run by OPMs. As more degree programs have gone online (driven, in part, by the success of the OPMs themselves), the cost of advertising using relevant search keywords Google AdWords has gone up. Because demand for them has gone up.

MOOCs are attempting to disrupt Google AdWords in education.

University stakeholders know this. Sort of. If you search the internet for articles about the cost and revenues, you won’t find anything published more recently than about 2015. After the first few years, they just stopped talking about costs and revenues. That shift wasn’t random. And of course, everybody knows how bad MOOC completion rates are and how badly they’ve failed to demonstrate consistent educational effectiveness under rigorous testing.

When I’ve asked folks I know who are directly or indirectly with MOOC programs at their universities why their institutions are still creating and maintaining these things, I typically get one of two answers. The first is that their bosses think it’s good marketing for the institutions despite the fact that they have data showing that YouTube videos work better. The second is that they frankly don’t know why they are still doing it.

By extension, Coursera is now an OPM. If it weren’t, then its underperformance in its relatively new online degree unit wouldn’t cause such a precipitous plunge in its stock price.

But it gets worse

If MOOCs turned out to be infomercials and everybody understood that to be the case, that would be disappointing but not the end of the world. Some of us never expected them to be the magic bullet.

The problem is that Coursera’s degree programs are also MOOC-based and 2U is making worrying (though admittedly cryptic) comments suggesting that they may be moving in that direction as well. I’ve seen no good data on MOOC-based degree completion rates. Or on MOOC-based degree efficacy. Or on the perceived value of MOOC-based degrees by employers. We do know how individual MOOCs perform on these measures: badly.

The only difference I can see between a MOOC and a MOOC-based degree is that students will be paying significantly more for them. Will this make a difference? Eh, maybe a little. I once had a conversation with Andrew Ng and Daphne Koller about research indicating that students would more highly value and be more likely to complete a course that cost $1 than one that is free. Maybe cost will matter because students will be literally invested in their education.

But that’s a thin reed on which to bet the future of billion-dollar companies, whose future is in turn paid for by students who are participating in an uncontrolled experiment that they are paying for. It seems more likely that if 2U joins Coursera on this path they may have to change their motto to “No Front Row.”

I get that universities need to develop more sustainable business models. pumping up degree programs through MOOC marketing and then lowering the price of those degrees by delivering them as MOOCs strikes me as a particularly risky way to try to meet financial goals, even if they’re willing to play fast and loose with their mission goals and institutional brands.

Michael, great commentary, of course. I would say a couple of things: one there is some good data from reputable researchers around what GA Tech is doing with “MOOC-style” masters programs (you note above there is none). Those may be an anomaly, and show that doing it right requires millions in initial investment. But a bigger point is this: Coursera (and EdX) have always skirted the “safe zone” by trying to be hype to investors but downplaying their significance on campus as to not frighten us. Coursera’s programming is as much about what universities decided to do with the platform as it is their “Silicon Valley zeal.” I remember consulting at one university faculty debate in 2014 on whether these **should** be moved to the university marketing department!! MOOC providers have evolved based on what their B2B consumers wanted and were willing to do – we never really pushed to make them meet our mission….if we had, would the reality have been too much for VCs to stomach?

GA Tech doesn’t call their programs MOOCs. They call them “Affordable Degrees at Scale.” And they currently run on Canvas. I’m not sure if their economics would have worked for the MOOC companies. I suspect not. But we’ll never know. And their decision not use a MOOC platform is also telling.