UPDATE: In the section on ‘Cash Cow vs. Growth Potential’, my choice of words could have caused misunderstanding. I did not mean to equate Operating Income with Cash Flow, and my choice of the word ‘cash’ in this section should really have been ‘income’, as my analysis was obviously based on Operating Income. I have made this correction below. My apologies for any misunderstanding.

Consider the recent news this summer that private equity firms have agreed to acquire both SunGard Higher Education (SGHE) and Blackboard in separate deals:

- Two market leaders in technology solutions for education,

- both generating revenues of several hundred million dollars per year,

- both business strategies at risk due to eroding market share in their core business since 2007,

- both facing challenges to integrate product lines and offer a clear road map for customers,

- and both sold to private equity firms for more than $1.6B.

SunGard Higher Education (SGHE) and Blackboard – brothers in arms.

At first glance, there are some strong similarities between the acquisition perspectives of both market leaders, but if you look deeper, the differences provide a good insight into the future of technology markets for higher education. These differences can explain why the ERP market seems to be consolidating with fewer choices while the LMS and educational technology market seems to be expanding with more choices.

Cash Cow Income Machine vs. Growth Potential

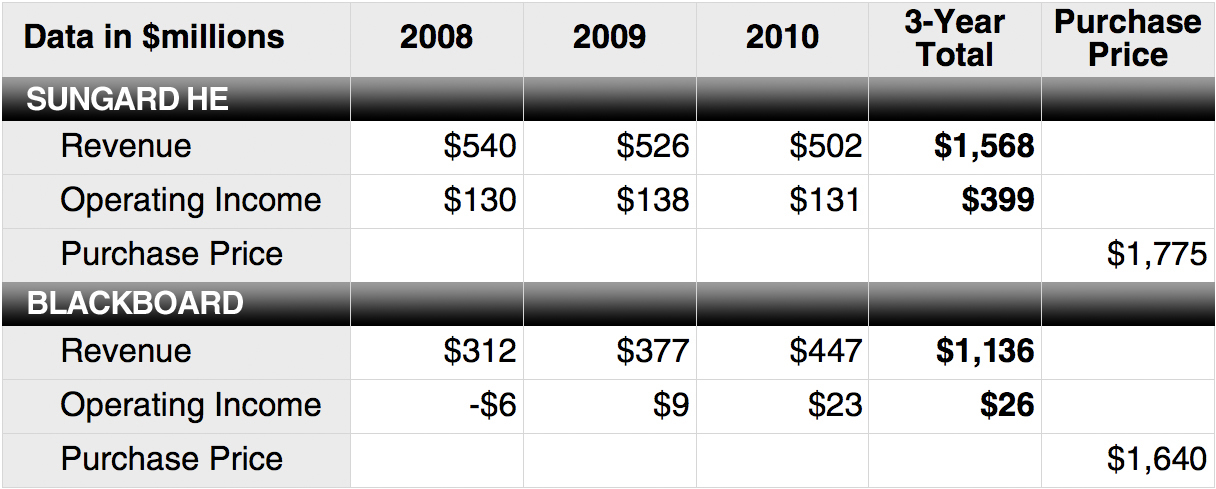

During research for this post, I was surprised to find out how much cash income that SGHE generates and how close Blackboard has come to SGHE’s revenue numbers. While Blackboard has seen its revenue increase due to corporate acquisitions of its own, it has only had a combined operating income of $26M over the past 3 years. In that same time, SGHE has seen its revenue decrease by almost 10%, but it has had a combined operating income of $399M.

It is somewhat difficult to compare the financials of the two companies, as they employ different accounting methods, so use the following table to see the big picture rather than the details. I have attempted to show total revenue (numbers are fairly solid) and operating income (not as solid), while ignoring provisions for income taxes. This data is based on SunGard’s annual report for 2010 (p. 36 as printed) and Blackboard’s annual report for 2010 (p. 26 as printed).

If Hellman & Friedman can achieve reasonable efficiencies by combing SGHE with Datatel, this investment could potentially justify itself in 5 – 7 years by focusing on cash flow operating income, even without SGHE finding a way to reverse its decline in revenue.

Blackboard, by contrast, has not yet shown itself to be a strong cash income-generating company; therefore, Providence Equity must be banking on strong growth to justify its purchase. I have already called out here, here and here why I think this growth is highly questionable due to Blackboard’s decline in its core business. If Blackboard does not continue its growth, and it faces increasing price pressure, then there may be serious problems with operating income justifying the purchase, as Jim Farmer has also suggested. The Blackboard purchase only makes sense [to me] if the company grows and increases in value.

ERP vs. Educational Technology Markets

While administrative technology and Enterprise Resource Planning (ERP) systems have had significantly higher budgets in the past than educational technology (defined loosely as systems and services that directly impact instruction and learning), it is apparent that the situation is changing. The market momentum favors educational technology along with LMS as the core application. Blackboard has done well to focus on these growing markets, whereas SGHE has been focused on ERP.

The ERP market is fairly mature, as others have described quite well, and market consolidation is an effective strategy to protect market share and pricing. There will be fewer competitors in 2012 than there were in 2010 for ERP markets. The most interesting higher ed ERP market change is the Kuali project – community source administrative systems in a similar structure as Sakai. While Kuali could prove to be a real game changer, the market has not developed yet. Mature markets are great for generating cash for vendors but not so great at transforming the business of customers.

The educational technology market is entering a new phase best characterized as a disruption (see previous post). There will be more competitors in 2012 than there were in 2010, and there is clear innovation being unleashed by new investments. Open source and community source systems are fully viable options already proving their worth at large and increasing numbers of institutions.

While both the ERP and educational technology markets have massive private equity deals (SGHE and Blackboard), these acquisitions should really be seen as changes in ownership rather than new investments. However, the educational technology market also has new investments occurring and affecting customer choices. Venture capital dollars are starting to flow into the market, and new companies are being created. Beyond venture capital, publishers and foundations are investing heavily in delivery systems (e.g. MyLabs from Pearson, MindTap from Cengage), creating new partnerships with LMS providers (Blackboard / McGraw-Hill partnership), figuring out how to engage in open educational resources, not to mention new concepts like Khan Academy. In short, there appears to be new investment in the educational technology market in a way that does not exist in the ERP market.

Markets Based on Transformation Potential

Even with the mature ERP market, there may be new choices for institutions. As my colleague Jim Ritchey has written, the SGHE / Datatel combination may add some real value to institutions. ERP players are attempting to broaden their scope and focus on CRM, enrollment management and peripheral systems. As necessary and important as ERP technology is, however, it is not seen in general as having the potential to transform future education.

In a recent Chronicle of Higher Education survey, CFOs focused on faculty productivity as the biggest financial opportunity for transformation at colleges. Educational technology has the potential to impact faculty productivity in ways that ERP systems cannot. The opportunity for transformation surrounds academic delivery and interaction. From the Chronicle article:

That the CFO’s focused on faculty productivity is a “really good window into the reality of the business model of colleges,” said John C. Nelson, who heads the higher-education practice at Moody’s Investor Service.

“That’s the last big area where there are really material efficiencies” to be had, noted Mr. Nelson. Since the financial crisis hit, in 2008, many institutions have been overhauling purchasing, instituting energy-savings programs, curbing costs on maintenance of buildings and grounds, and “attacking the costs of staff,” he said, but they haven’t changed how the biggest corps of their employees spend most of their time. “It’s the last area to go for really significant productivity gains.”

While I would argue that administrative bloat is another area ripe for creating efficiencies, this view from the CFOs backs up what the markets are indicating – that educational technology is seen as having the potential to transform education. This is a key reason why there is new investment in educational technology and why there are more vendor choices emerging, as described in a previous post of mine looking at overall market data.

In my mind, money is entering the market where transformation is possible – transformation to online and hybrid learning, transformation of the publishing model, transformation of the LMS space. Where technology is merely preserving or strengthening the status quo, budgets are down and vendors must protect their cash flows. This is why we are seeing market consolidation in ERP and market expansion in educational technology.