2U, the online service provider that went public in the spring, just released its financial report for the first full quarter of operations as a public company. The company beat estimates on total revenue and also lost less money than expected. Overall, it was a strong performance (see WSJ for basic summary or actual quarterly report for more details). The basics:

- Revenue of $24.7 million for the quarter and $51.1 m for the past six months, which represents year-over-year increase of 32 and 35%;

- EBITDA Losses of $7.1 m for the quarter and $10.9 m for the past six months, which represents year-over-year increase of -2% and 12%; and

- Enrollment growth of 31 – 34% year-over-year.

Per the WSJ coverage of the conference call:

“I’m very pleased with our second quarter results, and that we have both the basis and the visibility to increase all of our guidance measures for 2014,” said Chip Paucek, 2U’s Chief Executive Officer and co-founder. “We’ve reached a turning point where, even with continued high investment for growth, our losses have stopped accelerating. At the midpoint of our new guidance range, we now expect our full year 2014 adjusted EBITDA loss to improve by 17% over 2013. Further, we’ve announced a schedule that meets our stated annual goal for new program launches through 2015.”

The company went public in late March at $14 / share and is still at that range ($14.21 before the quarterly earnings release – it might go up tomorrow). As one of only three ed tech companies to have gone public in the US over the past five years, 2U remains worth watching both for its own news and as a bellwether of the IPO market for ed tech.

Notes

The financials provide more insight into the world of Online Service Providers (OSP, aka Online Program Management, School-as-a-Service, Online Enablers, the market with no name). On the conference call 2U’s CEO Chip Paucek reminded analysts that they typically invest (money spent – revenue) $4 – $9 million per program in the early years and do not start to break even until years 3 – 4. 2U might be on the high side of these numbers given their focus on small class sizes at big-name schools, but this helps explain why the OSP market typically focuses on long-term contracts of 10+ years. Without such a long-term revenue-sharing contract, it would difficult for an OSP to ever break even.

As the market matures – with more competitors and with schools developing their own experiences in online programs, it will become more and more difficult for companies to maintain these commitments from schools. We have already seen signs over the past year of changes in institutional expectations.

2U, meanwhile, has positioned itself at the high-end of the market, relying on high tuitions and brand-name elite schools with small classes. The company for the most part will not even compete in a Request for Proposal process, avoiding direct competition with Embanet, Deltak, Academic Partnerships and others. Their prospects seem much stronger than the more competitive mainstream of OSP providers.

See the posts here at e-Literate for more background.

2U has changed one aspect of their strategy, as noted by Donna Murdoch on G+. At least through 2012 the company positioned itself as planning to work with one school per discipline (or vertical in their language). Pick one school for Masters of Social Work, one for MBA, etc. As described in Jan 2012:

“As we come into a new vertical, 2tor basically partners with one great school per vertical. We find one partner, one brand that is world-class. We partner with that brand over a long time period to create the market leader in that space for that discipline.”

2U now specifically plans for secondary schools in different verticals as can be seen in their press release put out today:

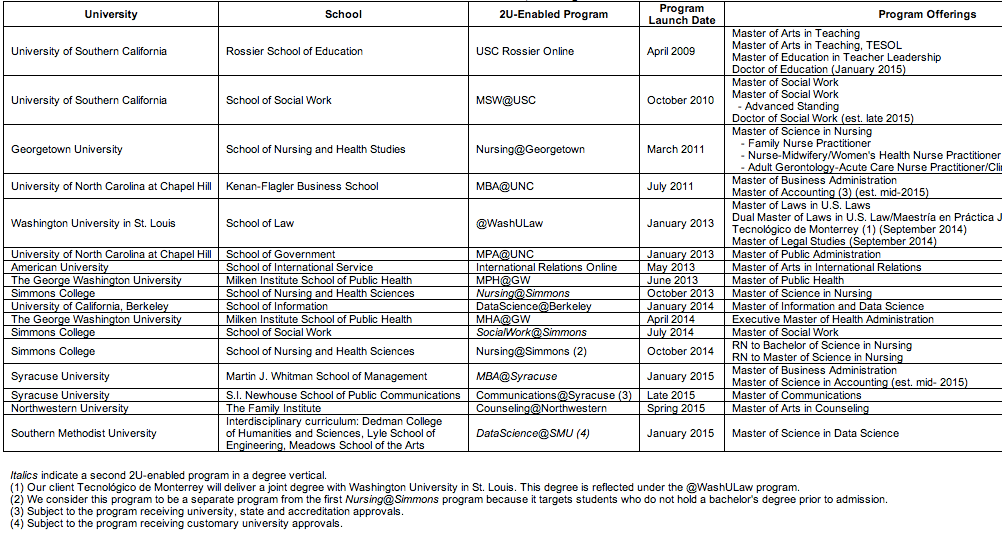

Note the duplication of Social Work between USC and Simmons, Nursing between Georgetown and Simmons, and Data Science between Berkeley and SMU. Note the new approach from page 20 of the quarterly report:

As described above, we have added, and we intend to continue to add, degree programs in a number of new academic disciplines each year, as well as to expand the delivery of existing degree programs to new clients.

View Into Model

Along with the first quarter release (which was not based on a full quarter of operations as a public company), 2U release some interesting videos that give a better view into their pedagogical approach and platform. In this video they describe their “Bi-directional Learning Tool (BLT)”:

This image is from a page on the 2U website showing their approach, with a view of the infamous Brady Bunch layout for live classes (synchronous).

We’ll keep watching 2U and share significant developments as we see them.

[…] Learning Platforms” that includes University of Phoenix, Coursera, edX and OpenEdX, 2U, Helix and Motivis (the newly commercialized learning platform from College for […]