With reporting contributions from Jeanette Wiseman and O’Neal Spicer

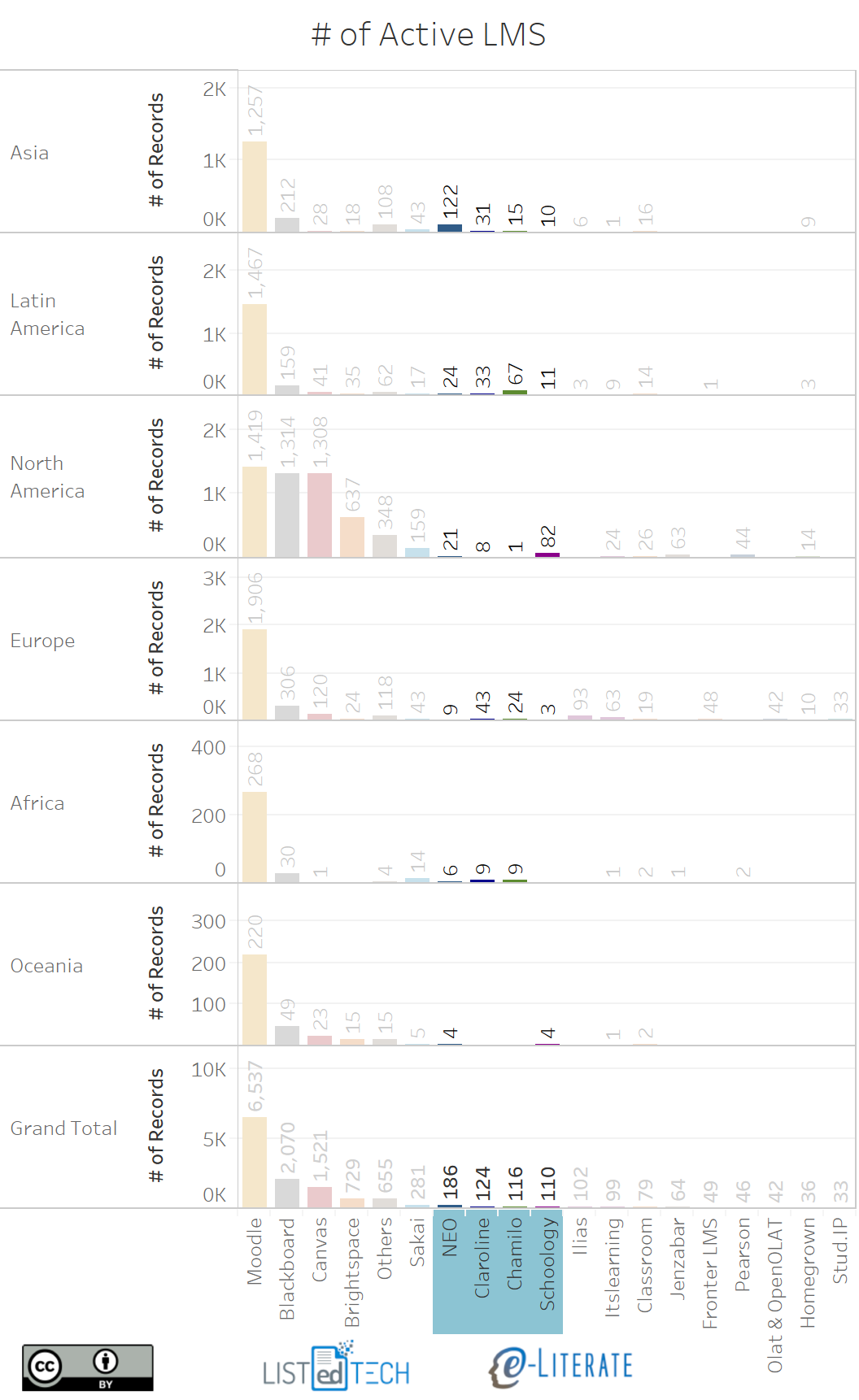

We have described how the global LMS market is converging in the sense that the Big Four – Moodle, Blackboard, Instructure, and D2L – end up being the primary competitors in more and more global regions, often with similar dynamics. We have also described Sakai and its decline in some detail. But what about the next level down? Let’s consider four LMS solutions that are still quite active but with fewer institutional users than Sakai – Schoology (whom we have described before), NEO, Claroline, and Chamilo. ((Disclosure: Blackboard, Instructure, D2L, and Schoology are subscribers to our LMS Market Analysis service. Blackboard, Instructure, D2L, and Pearson are sponsoring participants in our Empirical Educator Project.)) The following graphic shows both primary and secondary system usage in higher education in six different global regions, and all four systems have more than 100 active implementations.

Schoology NEXT

- The Schoology NEXT conference occurred at the same time as BbWorld this year. This is a mostly K-12 conference – as that is the primary market for Schoology – with a different attendance demographic than most LMS conferences with the majority of the attendees being actual classroom teachers or instructional designers, not the typical administrators or IT staff that you see at the other user conferences. This audience is more focused on the use of technology to enhance teaching and learning in their classrooms, to assist with assessment, or to fill a requirement of use of technology for professional development. The break-out sessions reflected this academic focus.

- The only new features or development that were discussed at any length during the keynote presentations involved the vague promise of “Personalized Learning” support. There was little information about what new features would look like, what they would encompass, or if they would entail additional charges like Schoology’s assessment platform. In an interview with CEO Jeremy Friedman and the new President Justin Serrano, they said that the vagueness is by design. The company is still working through their users’ needs and will be completing development on those features once that assessment was complete.

- When discussing if the company saw Google Classroom’s continued growth in the K-12 market as a threat, Friedman said it is the opposite. They see that in K-12 space Google Classroom fills a need for a classroom, a school or a district that are dipping their toes in the LMS space, and once the school starts actively using the technology they quickly outgrow it. In these cases, Schoology sees Google Classroom as seeding the market for them, and they actively target those Google Classroom schools. In most cases, if responding to an RFP, it will be Canvas they will be up against. Rarely do they see Blackboard or even Moodle in these situations. They feel like, and this was reiterated by their users, that one of the most significant benefits that Schoology users see in the platform is their ease of use. The interface is reminiscent of Facebook; it is familiar to the teachers they quickly can navigate and load announcements and content to their site with very little training or IT support. It may not carry with it the bells and whistles of a Blackboard Learn or even Canvas by Instructure, but for what these K-12 teachers need, it fits the bill. For now.

- Regarding targeting customers in higher education, the company stayed the course from January 2017 in which they will continue to support their higher education customers and will take easy sales opportunities, but are not planning to aggressively pursue that market. While this strategy only lightly targets higher education, Schoology has over 100 clients at universities and colleges worldwide – mostly small private schools, and often as secondary systems – using their platform. Customers using as a primary system include Wheaton College and Saint Vincent College in the US and the Universidad Metropolitana de Monterrey in Latin America. Schoology is also used as a secondary system at schools including UC San Diego.

NEO, Claroline, and Chamilo

The other three systems – NEO, Claroline, and Chamilo – are important in the global market, even if most academic buyers (in the US, at least) likely have not heard of them. All have more than 100 higher education implementations worldwide.

- NEO is the academic LMS from Cypher Learning: Based on our conversations at the K-12 focused ISTE conference this summer, Cypher Learning has 60 employees and claims 2 million customers worldwide (combining NEO with the Indie and Matrix LMS for corporate markets). In higher ed, their largest implementation is with STI College in the Philippines with a systemwide deal that gives them 77 campus adoptions. The system has been designed native to the cloud and boasts a fairly intuitive user interface that addresses competency-based education and mastery learning.

- Claroline Connect is an Open Source project run out of France: This system – which has the greatest adoption in Europe, Latin America, and Asia – is a second-generation open source project. In the early 2000s, the University of Lyon and the Université catholique de Louvain created two open source LMSs, and subsequently Claroline Connect combined these projects into the current system based on more modern technology. Get your French ready, or use captions.

- Chamilo is an Open Source project run out of Spain: This system, used most often in Latin America and Europe, also has origins in the predecessors to Claroline, forking into the Dokeos project and then forking again to Chamilo in 2010. The system is supported by official supporting vendors in the following countries: Belgium, Spain, Italy and Germany. The Belgian company also has offices in Peru. Again, get your French ready.

While we have only described this second tier of global LMS providers in broad strokes, we hope this post gives a richer view of the broader LMS market and available systems.

Hi, nice to see Chamilo starting to appear in the list. I’d like to point out that the numbers collected by ListEdTech are self-collected, and are just slightly more precise in the U.S. than they are abroad (for obvious language and ListEdTech-fame-related reasons).

Once these “new” platforms start to put more energy into marketing in the U.S., these number might move considerably (in the extra-long time frame of LMSes).

The main reason they have not entered this market yet is because there is no space for movement with the current giants there, spending hundreds of millions in marketing each quarter.

Investment in LMS platforms in Europe is nowhere near the US’s, and South America has an education system that tries to mimic the US’s but with much lower budgets.

If things go sour for Blackboard and/or Instructure (as per your other recent article), there would be a tremendous opportunity for growth. In any case, it will be interesting to watch or participate in.

Hi Yannick, You are right that our data is more complete in US while we develop international market data over time. This is why we typically show %s instead of raw numbers, but in this case it seemed important to give some sense of relative numbers between regions. Thanks for insights on how you see the market progressing, and opportunities that may arise.