One subject that we have not covered much at e-Literate lately is the market position of Moodle. Given the significant LMS market changes over the past two years, it might be worth considering how institutions are adopting and using Moodle. In the US at least, there has been a significant change – whereas in previous years Moodle growth came primarily from institutions moving away from Blackboard, today much of the growth appears to have shifted to online service providers.

Traditional US Market

From 2006 – 2011 Moodle grew quickly in the US, both in terms of the number of users (students, faculty) and in terms of the number of schools adopting Moodle. This growth appears to have slowed considerably since 2011, although the data can be difficult to interpret since the system is open source – anyone can download for free and run Moodle, without even notifying Moodle headquarters or often the institution.

While the data is inconclusive, my assumption is that traditional Moodle growth – institutions adopting the LMS as the campus standard, typically moving away from Blackboard or WebCT – has significantly slowed from its peak growth in 2009 – 2011. I’ll write a separate post on this subject in the future.

New Growth Model

While the traditional growth may have slowed, there is a market segment in the US where Moodle is quietly dominating – as the preferred learning platform (or LMS) for online service providers.

Online service providers are organizations (mostly for-profit companies, but with at least one non-profit variation) that help non-profit schools develop online programs. These providers, also known as online enablers, online program management or school-as-a-service, provide various services for which non-profits institutions typically do not have the experience or culture to support. Some examples of the services include marketing & recruitment, enrollment management, curriculum development, online course design, student retention support, technology hosting, and student and faculty support.

The Parthenon Group last year reviewed this growing market for nonprofit institutions, including a summary of the largest online service providers.

What has sparked this increase in online enrollment at non-profit institutions? Choosing not to “reinvent the wheel,” many non-profit institutions have partnered with online enablers like Embanet, Bisk, Deltak, and Pearson that provide institutions the blueprint and support to transition into online learning. More importantly, these companies offer schools a full value chain of services (e.g., course development, IT support, recruiting/marketing, processes,

and cycle times) that are quite different from traditional non-profit strategies.

It is this market where the Moodle LMS has seen its most impressive growth in the US in the past two years, as approximately half of these providers use Moodle as their core learning platform. Typically the companies customize the platform by extensions to Moodle and white labeling. This market is interesting, as the companies themselves are growing, leading to organic growth in LMS usage.

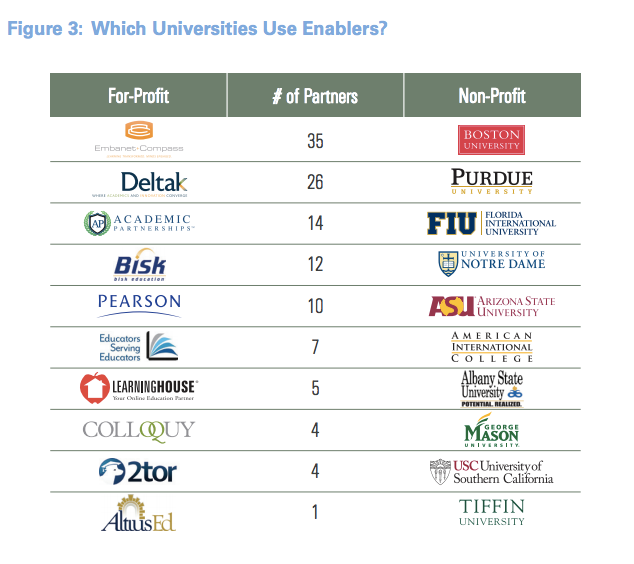

I took the list above from Parthenon (which is now 9 months out of date, but still captures the biggest players in this market), and added a few more companies. Some of the information below is based on the CalState RFP process and associated documentation.

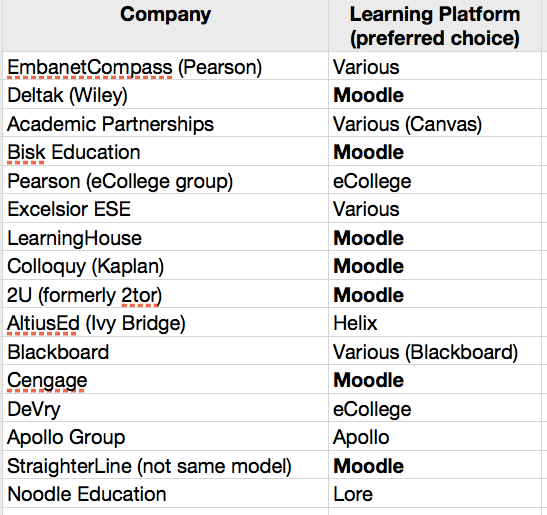

- EmbanetCompass, which was acquired by Pearson in October 2012 for $650 m, is officially agnostic on learning platforms, allowing the school to choose.

- Deltak, which as acquired by Wiley in October 2012 for $220 m, has built their Engage platform with Moodle as the foundation.

- Academic Partnerships allows schools to choose their own learning platform, but they provide Canvas as their preferred solution.

- Bisk Education provides Moodle as the core learning platform.

- Pearson’s eCollege group uses LearningStudio (formerly known as eCollege) as its learning platform.

- Excelsior’s Educators Serving Educators (ESE) is officially agnostic on learning platforms, allowing the school to choose.

- LearningHouse provides Moodle as the core learning platform.

- Colloquy, owned by Kaplan, uses Moodle as the core learning platform.

- 2U, formerly called 2tor, uses Moodle as the core learning platform.

- AltiusEd, the company behind Ivy Bridge College (recently losing its status as provider of online programs for Tiffin University), moved from Moodle to its own Helix learning platform. Ivy Bridge

- Blackboard, which has moved into online program management, is officially agnostic on learning platforms, allowing the school to choose (but I’m sure they’d prefer the use of Blackboard Learn).

- Cengage bid on the CalState online program using Moodle as its learning platform.

- DeVry bid on the CalState online program using eCollege as its learning platform.

- Apollo Group (owner of the University of Phoenix) bid on the CalState online program using its own Apollo technology as its learning platform.

- StraighterLine, which is technically not an online service provider, but they are a for-profit company that indirectly helps nonprofit schools benefit from online courses, uses Moodle as its core learning platform.

- Noodle purchased Lore to use its technology as the core learning platform.

This is impressive adoption of a single LMS choice, especially for a growing market segment. From the information that I have, these were independent decisions on the part of online service providers rather than a coordinated push by Moodle or its partners.

And did I not hear that Blackboard are moving to becoming a full-service provider and is now agnostic on platforms (well they bought Moodlerooms)?

Moodle may have become dominant here but the CalState selection document notes Moodle as a negative when rating the providers that use it. All Moodle users were eliminated before the finals.